In this post I will detail the business model innovation analysis I did for a startup founded by Yaron Samid- BillGuard. This assessment of BillGuard’s current strategy was conducted using the tools and concepts from MBA295M, Business Model Innovation and Entrepreneurial Strategy taught by the mercurial Prof. David Charron, a successful entrepreneur in his own right. The goal of this analysis is to project a true picture of firm offerings, sources of sustainable competitive advantage, network effects, market conditions and fragmentation, competitive positioning, pricing strategy and recommendations to improve its business viability.

BillGuard is an early stage consumer finance protection startup. A description of BillGuard’s company and business model provides a common understanding of the central value proposition, as well as the company’s primary strengths and weaknesses. BillGuard detects fraudulent, deceptive and erroneous charges on credit and debit card bills. Users register for the service by linking their accounts to the BillGuard system, which scans all transactions and issues a warning to the user if suspicious transactions appear on the bill. The service is described as “people-powered antivirus”, due to the crowd-sourcing approach to detecting fraud or errors. A proprietary algorithm scans transactions previously submitted into the system by other users, monitors complaints on websites and social media sites like Twitter and Facebook, and analyzes individual transactions for factors such as location or merchant history. In a second step, BillGuard harnesses the knowledge of its customers. When the system detects questionable charges, it notifies the credit card holder and asks for it to be reviewed. If a transaction is disputed, the algorithm records it as such and warns other credit card holders who have the same or similar charges. As of October 2012 BillGuard claimed to have identified $1M in unwanted charges for their customers. It is hard to justify this claim because it can be safely assumed that most savvy users of the internet do not have much to complain about in their card statements. There are, however, certain segments of credit card users like the very young and the very old who do not exercise scrutiny in conducting transactions online. These segments are good sources for BillGuard to source fraudulent transactions from thereby adding to its internal database of fraudulent merchants.

The service is also available for banks as white label integration into existing infrastructure. Alongside fraud monitoring and detection, BillGuard offers resolution management for disputed transaction, cutting down the bank’s processing costs and increasing convenience for customers. The company has declared that their roadmap includes expanding their crowd-sourced complaint detection platform to other services and payment providers, such as cell phone bills and e-payment solutions.

BillGuard was founded in April 2010, and launched their service to the public at Techcrunch Disrupt in May 2011, where it ranked second in the StartUp Battle. They earned a lot of attention in mainstream and tech media such as ABC News, Wall Street Journal, NY Times and Wired Magazine, and also received a number of awards by financial services organizations.

Two months after founding the company, BillGuard raised a $3M Series A round from SV Angels (Ron Conway), Bessemer Venture Partners and other investors. The second, $10M round closed in October 2011 which was raised by the previous financiers and added Saul Klein and Eric Schmidt to the investor panel. For a company at this early stage (Series A 2 months after founding) and in this sector, both rounds were substantially above the average size of each respective round. The company currently has about 30 employees with offices in New York and Tel Aviv.

Yaron Samid, co-founder and CEO, is the driving force behind BillGuard. He is a three-time entrepreneur in the consumer tech sector and sits on a number of boards of technology start-ups. He previously co-founded Pando, a service with over 50 million users worldwide, and has experience in product marketing and product management. Raphael Ouzan, co-founder and CTO, leads the product and R&D office in Tel Aviv, and a team of data scientists, mathematicians and engineers. BillGuard’s advisory board is comprised senior experts in big-data, payments and financial services such as Tim O’Reilly and Scott Lofteseness, EVP at VISA.

BillGuard’s Business Model

BillGuard has relationships with three customer groups: Consumers, Banks and Merchant.

Consumers- BillGuard scans the transaction activity of its users, running them through automated tests that identify suspicious charges. BillGuard also checks consumer complaint websites and social media for mentions of the merchants and charges. BillGuard will identify misleading charges, billing errors, scams and fraud and notify users via email when attention is required. When users login to BillGuard, they can verify any questionable transactions. If they find a charge they want to dispute, they can submit the charge to BillGuard’s Transaction Resolution Center, and BillGuard will contact the merchant on the user’s behalf to resolve the dispute directly. Any user activity is used by BillGuard to help identify unwanted charges on other user’s accounts. BillGuard for consumers is a fermium model. It is free for up to 3 cards. BillGuard Family protects 10 cards for $79 per year. BillGuard also provides a Business Plan, though pricing is not made public.

Banks- BillGuard provides an integrated solution for online cardholder resolution management and card protection systems. A bank can elect to offer BillGuard bill monitoring to its consumers, using BillGuard’s complaint and transaction analytics to identify unwanted charges, and also manage the consumer inquiry and dispute process. Banks benefit from integrating with BillGuard by improving their quality of service while lowering their inquiry and dispute processing costs.

Merchants- When a consumer interacts with a transaction through BillGuard, the service maintains a record and creates metadata around the transaction so other users can understand why each transaction appears. When consumers choose to dispute a charge, BillGuard contacts the merchant directly and gives the merchant the opportunity to resolve the complaint without going through the banks, which is usually very costly. Merchants get a consolidated view of what other consumers are saying about them, and a rating of their transactions by BillGuard users.

Value Proposition

The central idea of BillGuard started when a friend of the founder, Yaron Samid, called him to inform him of a fraudulent charge that he had received. Samid would never have found this charge himself – like 90% of Americans, he rarely looks at his statements. But it only takes a small and active minority to identify these charges for everyone. Samid realized that unwanted charges could be identified in the same way spam was finally controlled by email companies – by asking users to flag it. This is happening already –10,000 billing complaints are pouring into bank and credit card call centers every day, plus millions more post complaints online to the Better Business Bureau, Yelp, and social media. According to BillGuard, Americans will lose an average $300 per year on hidden charges, billing errors, and forgotten subscriptions. An estimated $7B will be lost this year due to fraud, though banks will only catch one third. The idea they are banking on is that users are interested in receiving alerts whenever someone else reported a suspicious charge that also appeared on your statements.

Revenue Streams

As a freemium business, BillGuard currently has one major source of revenue: consumers that upgrade to protect more than 3 credit or debit cards at a price of $79 per year. They also expect to collect SaaS license fees for bank or credit card companies that integrate BillGuard with their billing system. The company has not publically stated any corporate partners at this stage. BillGuard has also indicated a desire to charge merchants for the right to display the BillGuard logo on their site, but no public statements have identified any merchants paying for this service.

Analysis of the BillGuard Business Model

Competitive Landscape

The market for fraud detection is crowded with several B2B players. Memento Security offers a portfolio of fraud detection solutions for checks, ACH/wire and credit card fraud detection. Accertify’s Interceptas platform provides a data-mining based solution to fraud-management. Iovation’s web-fraud detection platform is unique in the manner in which it uses device-recognition to detect and eliminate fraud. There are several customer segments each of the incumbents target, namely commercial enterprises that have a heavy online transactional component, banks who hold deposits and non-financial institutions that need data compliance and risk management solutions. It is fragmented market with a large player, American Express owned Accertify, and several smaller players.

The incumbents sell products and services to banks and corporations that have a significant online transaction component to their businesses. Consumers do not pay directly to these providers. BillGuard, however, is the first B2C player in this market and charges $79/year for monitoring more than 3 credit cards. They also have an offering for businesses that is most likely priced based on WTP since this price is not published. Using this model, BillGuard is attempting to disrupt the business model of the incumbents, which relies on an enterprise-sell. BillGuard’s B2C approach coupled with its affordability as a fraud management platform might give it a wedge in the market but is not going to sustain substantial growth. Incumbents have key partnerships and technology value propositions that are hard to match and beat. BillGuard’s value proposition is strong to users but its ability to execute is relatively weak given that it relies heavily on crowd sourced content and does not rely on the risk metrics that are used by the incumbents to provide fraud detection. BillGuard’s competitive positioning is shown in the strategy canvas [Exhibit 1].

Memento has strong investigative capabilities from their partnerships with analytics providers such as IBM. Accertify partners with several analytics and risk-metrics provider such as Targus and ID-Analytics, and moreover they are a wholly owned subsidiary of American Express which gives them access to complaints data making their proposition even stronger. Over the long term BillGuard should look to strengthen its fraud-detection platform via a technology acquisition, such as that of Id-Analytics, which provides an enterprise-grade risk management and customer analytics platform.

Analysis of Consumer Pricing Plans

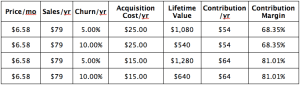

Using the simplistic customer lifetime value formula: [Monthly Sales] x [% contribution-margin / % churn-rate] we can compute the CLV for BillGuard’s customers. Assuming a $25 acquisition cost, a conservative 5% churn rate per year (the actual could be higher) the lifetime value of 1 customer is $1080, as shown below. I have modeled the CLV on churn rate and acquisition costs to present different CLVs that are possible.

The worst-case scenario is $540/customer with a churn rate of 10% and acquisition costs of $25, and $1280/customer if the churn rate is 5% and acquisition costs drop to $15. In order to return an ROI of 5x on investment ($13M) to their investors within 5 years, BillGuard needs 60,000 paying customers with a CLV of $1080 each, on average. If we assume 20% customers actually sign up for the $79 per year pricing plan, then the number of users of BillGuard needed are approximately 300,000 over 5 years. This equates to 60,000 paying customers of the service each year with some room for error.

However, it does not appear that BillGuard.com is registering 60,000 or more unique users each year. BillGuard.com has an Alexa rank of #323,884 which is better than Accertify.com and MementoSecurity.com but it lags way behind Visa.com and Mint.com. Mint.com offers credit card, bank account and investment asset aggregation dashboards and reporting capability to users, is owned by Intuit and is a fast growing company.

BillGuard receives 31,500[1] unique visitors monthly but it is hard to say if these website visitors actually sign up since BillGuard has not released such numbers publicly. Still it can be said that these are very low numbers when compared to Mint.com, which see 600,000 non-unique visitors each month. If we assume a 10% conversion rate, then approximately 3150 users will be signing per month, which equates to about 38,000 users per year. Hence it is probably hard for BillGuard.com to complete a 5x return to their investors in 5 years. As such, the current pricing model and market entry strategy is not satisfactory.

BillGuard Estimated Web Traffic

Source: compete.com

Google Trends Mint.com vs. BillGuard.com

Source: google.com/trends

We recommend BillGuard change its pricing model to skim the market of the much more risk-averse customers who will have much higher WTP than the more risk-tolerant credit card users who will not want to pay more than $79 per year.

Scaling issues

As noted in the analysis above, BillGuard needs to acquire more customers quickly. A market-skimming price strategy needs to be followed for the customer segment that has a higher WTP, however, BillGuard cannot afford to ignore the low WTP customer segments as well. It has to balance profitability and growth but the focus must be growth. BillGuard must press the growth accelerator by doing more market research to identify and narrowly target the risk-tolerant segment.

The market for credit card fraud detection, fraud reporting and resolution is huge. In a B2C model, it is practically the entire population of the world that uses credit cards. This is not an overstatement because BillGuard’s sales pitch is exactly that: help credit card users detect hidden fees, spurious recurring charges assisted gladly by the rest of the credit-card user community. There is a strong network effect here that BillGuard can capitalize on if it is able to scale quickly while maintaining a healthy P&L.

The BJ Fogg Behavior Change suggests that BillGuard should be able to initiate consumer behavior change to use their service by using a trigger. Although not all consumers may be highly motivated to initiate using BillGuard’s service, it is extremely easy to do for any consumer that uses online banking at a major US bank, or has used Mint.com. BillGuard needs to determine what an appropriate and cost effective trigger should be to capture the attention of low motivation users.

In terms of transaction volume of credit card companies in the US, a quick lay of the land is presented here ranked on purchase volume:

| Rank | Issuer | Purchase Volume ($B) |

|

1 |

American Express |

$460.69 |

|

2 |

Chase |

$333.13 |

|

3 |

Bank of America |

$237.51 |

|

4 |

Citibank |

$192.48 |

|

5 |

Capital One |

$98.34 |

|

6 |

Discover |

$92.47 |

|

7 |

U.S. Bancorp |

$73.57 |

|

8 |

Wells Fargo |

$49.10 |

|

9 |

HSBC (now Capital One) |

$30.64 |

|

10 |

Barclays |

$29.80 |

|

11 |

USAA |

$28.24 |

|

12 |

GE Money |

$20.98 |

|

13 |

PNC |

$14.19 |

|

14 |

Cabela’s WFB |

$11.94 |

|

15 |

Target |

$8.55 |

Table 1: Purchase volumes of credit card companies

Source: http://www.cardhub.com

Today, BillGuard is trying to be a generic credit-card fraud detection platform. There is no evidence, given the public sources of information available, of it partnering with any credit card provider listed in the table above to drive more customers of that company to its platform. When I2c Inc., a payment processing company, was not getting enough traction with the market leaders, it decided to pursue Discover Card to become the credit card company’s payment gateway. Discover Card was lagging behind Chase, American Express and Visa in market share and needed a strong value adding partnership with a payment platform to extend its customer reach while ensuring safety and security of online transactions. The situation was a win-win that has thrived since inception.

We recommend that over the short-term BillGuard explore opportunities to partner with credit card companies that do not have sophisticated fraud-detection and resolution capabilities of their own, and other companies that have significant purchase volumes, and hence a large potential to create more signups on BillGuard.com.

Business Model Strengths and Weaknesses

Strength – Value Proposition

The strengths of BillGuard’s business model are its value proposition and the scalability of their product. First, the offering to credit and debit card holders is absolutely unique—no other competitor offers a similar consumer facing product yet, giving Yaron and his team a 2 year head start. The service is easy to use, non-intrusive and provides an additional layer of security to card holder. The value proposition for their B2B customers is also very convincing. BillGuard can offer a significant reduction in cost through minimizing processing cost of dispute resolution, which primarily happens in costly call centers, by allowing credit card users to resolve bad charges directly with the merchant. They also offer a unique way to detecting fraudulent and erroneous chargers adding an extra layer of security to the banks infrastructure.

Strength – Market Trends

Second, the markets they address with their value propositions are very likely to grow over the foreseeable future though a greater popularity of card payments with merchants (this is the particularly the case in non-US market), growth of e-commerce and the rise of other non-cash payment methods (such as mobile payments, NFC, etc.). Further, the product on it’s own is very scalable. The quality of the service actually improves with an increasing number of uses reporting bad charges. As with most tech-startups, IT infrastructure has become very affordable which reduces costs of growing the business. Also, their system can be applied to other types of bills such as cell phone bills, opening up other long-term growth opportunities.

Weakness – Technology

BillGuard’s biggest weakness is the technology behind their service. The problem they solve, doesn’t seem to be hardest technical challenges, and certainly one that can be solved by other experience engineers in the enterprise security sector too. It’s not based on primary research, nor is the idea of “people-powered” a unique principle. Also, on their website, they claim that they own intellectual property that protects their competitive advantage—or at least have patents pending. This usually doesn’t create a high enough barrier to entry for competitors or prevent copy-cats from using the same principles of people-powered fraud protection. Some people even argue that filed patents provide competitors with a blue-print and inspiration on how to solve the same problem.

A further issue with the underlying technology is the network effect it relies on to deliver a reliable service. If we imagine a situation, in which a large credit card company such as Visa, offers a similar, crowd-sourced security feature, their significantly larger customer base, will create a product of much higher quality than BillGuard’s in a very short period of time. Assuming that these organizations manage to create incentives for their customers to flag unwanted charges, a in-house solutions seems to be a better alternative for large organizations.

Weakness – Revenue Stream

The second weakness of the business model we identified is the revenue stream. Currently, the service is offered for free to customers with less than 3 credit cards. BG only makes money of customer who sign up for a $79 annual subscription. We believe this way money that customers are willing to spend is left on the table. The issue here is that BG charges for monitoring of the cards, however this is not where the value is created for the customers. So rightfully, they offer it for free to most customers. When a bad charge is discovered the customers suddenly has much clearer willingness to pay. For example, a customer has only one card and only one bad charge of a few hundred dollars. Finding this charge is free for the cardholder, however presented with the discovery, most customers would be willing to pay for this service as share of the money they saved.

Assessment of their potential success

In order to assess their potential of BillGuard becoming a successful company, we need to understand the implications of the VC investments in this firm. The venture capitalist’s and the entrepreneur’s interests are now aligned, and both work towards the goal of creating an exit opportunity with the common goal to maximize returns. An exit could be either an IPO, an acquisition or a merger. The time horizon for reaching those goal is based on the lifecycle of the investment fund which ranges from 5 to 10 years from inception; for online tech companies it’s usually at the lower end of this spectrum. In order to make an exit possible, revenues in the range of $50M-$100M should be reached within this time frame. Based on the information that is publicly available, it’s not possible to make a reasonable estimate on how well BillGuard is currently performing against these goals and if they are in track to liquidity.

Looking at the traction BillGuard gained with consumer, the figures are not convincing. In the last 12 month, the services saved $500,000 in bad charges (according to their website and other sources), which translates into less than 2,000 customers if we assume that an average customer loses $300 per year in bad charges and if we assume BillGuard would catch all these. Even if more prudent, the number of total charges of just over $1M saved through BillGuard seems small for a 36 month old service, that is free for most users.

An explanation for this lack of traction might be a lack of understanding of the need and the resulting willingness to pay. Since 9 out of 10 credit or debit card owners don’t check their bills, people are not aware that bad charges are an issue. It only becomes apparent, in case of serious fraud, which usually is covered or at least detected by the card company. Resulting from that is the consumers inability to see the value in the service BillGuard provides – for a customer who doesn’t check their bills, it’s not possible to estimate how much money they would save, which helps establish their willingness to pay. Although BillGuard identified a need and has a compelling value proposition, they have struggled to find their product-market fit.

A further concern regarding BG’s potential for success is the competitive landscape that they face with their B2B offering. Transaction security is amongst the top priorities of financial institutions and a growing billion-dollar market. As outlined in the analysis above, the competition in this industry is fierce, with specialized companies that have a significant market experience, highly skilled staff and a broad range of product and service tailored for this type of customer. It seems unlikely for BillGuard to take a significant share of that market, considering the high requirements for reliability, accuracy and customization in that industry. Further, customer acquisition is even more challenging at that scale.

On the other hand, BillGuard’s team, investors and advisors, suggest a much more positive outlook. The founding team can look back on previous successes, the investors are amongst the most prestigious in Silicon Valley and the advisors provide a broad knowledge as well an industry network. Considering that BillGuard managed to raise a substantial second round 16 months after Series A, it’s fair to assume that the company is on a convincing road to success. They also managed to build a reasonable buzz in press and amongst industry organization.

To come to a conclusion, we’re not too optimistic of the company’s chances of turning into an exitable business that yields satisfactory returns for their investors due to the reasons outlined above. However, the company is still young and has enough time and resources to improve their product for the B2B space, and build up traction with card holders.

Below are some specific recommendations that the company should implement in order to be successful.

Focus on Customer Acquisition

In the balance between growth and profitability, BillGuard needs to focus squarely on growth. At this stage, the company needs to be focused on acquisition. Big banks seem like an attractive target, but BillGuard does not complement their business model. Banks and credit card companies will quickly embrace technologies and features that increase consumer-spending rates, like mobile payments and rewards. BillGuard is a feature that banks could build themselves but have little incentive to do so. So BillGuard must focus on acquiring consumers itself, and grow organically and attempt to become a de facto industry standard.

To do so, BillGuard must focus on reducing any friction to customer acquisition. It must understand viral levers like network effects, and introduce viral features to its products. This is critical to get the acquisition costs down for the freemium model. It must also understand the BJ Fogg behavior change model, and identify triggers that will lead to consumer adoption.

BillGuard needs to determine how to create value for the everyday consumer, including the 75% of consumers who likely will never have an unwanted charge disputed and resolved through the product. This could be creating a greater sense of security or peace of mind for a consumer’s personal finances, helping consumers “fish for money” through insights into their transaction characteristics or other value that can be derived through channel partners. BillGuard needs to make consumers care about protecting their cards, in a more substantial way than they currently receive.

Revisit Pricing Strategy

A second fundamental change in BillGuard’s business tactics we recommend is to come up with an different consumer pricing model. As described in the weaknesses section, their current structure omits the willingness to pay by customers, once BG discovers bad charges and helps them to get their money back. We suggest a revenue model, that’s reflects the success-rate of their service—BillGuard charges a share of the amount of a bad charge they discover. This kind of performance-based fee structure work well in many other B2B and B2C settings and also aligns the interest of BillGuard with the interests of their customers. Instead of charging for a service that doesn’t create any tangible benefit for most of the time, our recommended pricing model captures value when value is created for the customer. Additionally, it signals that BG has confidence in their own system and also presents a more transparent pricing model.

To further enhance the willingness to pay based on this pricing model, we recommend BG to implement features that go beyond discovery of erroneous charges and actually manage the process of disputing and recovering the charges.

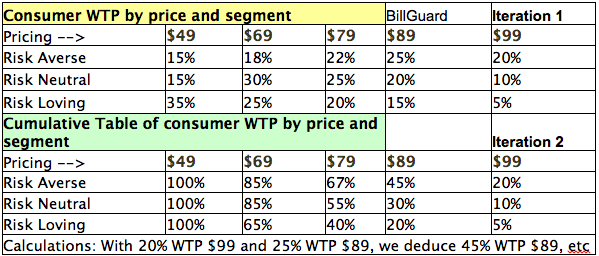

Along with the change in the pricing model, BillGuard should also look at it’s customer segmentation, identify those with a higher willingness to pay and understand how to create value for them. In particular, change the pricing model to skim the market of the much more risk-averse customers who will have much higher WTP than the more risk-tolerant credit card users who will not want to pay more than $79/yr. However, this is easier said than done. Extensive market research will be required to truly understand the motivations of credit card users and several iterations of analysis will need to be done to isolate risk-averse, risk-neutral and risk-tolerant segments. A WTP matrix should be constructed and segment-specific total revenues should be calculated at different price points. Further, this hypothesis should be tested in the market using several popular techniques such as surveys and focus groups. An example WTP matrix is presented here in Exhibit 2.

Create IP differentiation and protection

Third, we recommend they refocus on their technology. As outlined in the weaknesses section, the problem they solve currently is not a hard one, their IP is not strong enough to protect them from copycats, and potential new entrants can catch up quickly. First, the system needs to be more accurate and better in recognizing wrong charges. After having registered our own cards, BG found questionable charges that actually were correct and were made by reputable vendors. Also, currently the system hinge on power of the network of users. Since this is not a sustainable, long-term differentiator, we recommend broadening or improving other data sources that help with the detection of charges.

Plan for integrated, enterprise-ready technology

Over the long term we recommend BillGuard look to strengthen its fraud-detection platform via technology acquisition, such as that of Id-Analytics which provides an enterprise-grade risk management and customer analytics platform. However, chasing Id-Analytics or any of the other leading providers may not be a good idea since these entities already are in partnership with BillGuard’s competitors. Potential targets for acquisition are JanRain and LifeLock, both of which focus on providing bleeding-edge identity theft prevention technologies and would be a good complement to BillGuard’s credit-card fraud detection and prevention platform. Further, it would help BillGuard extend its platform to banks accounts, ACH/Wire protection and check monitoring.

Create Strategic Alliances

We recommend that over the short-term BillGuard beef up its technology and analytics platform. Having acquired this core competency, either through acquisition or building it themselves, BillGuard then needs to explore opportunities to partner with credit card companies that do not have sophisticated fraud-detection and resolution capabilities of their own. Credit card companies that have significant purchase volumes but without a sophisticated analytics platform will find value in partnering with BillGuard creating potential for increase traffic and paid usage at BillGuard.com.

US Bancorp and Discover Bank are good targets for alliance that BillGuard should explore. Discover, in particular, are known to be aggressive value seekers and partner with new market entrants more readily than do the other banks. An example cited earlier in this paper is Discover’s partnership with I2C payment systems to create value-added services such as transaction processing, stored-value card management and prepaid application services.

Exhibit 1: Strategy canvas showing competitive positioning

Exhibit 2: Willing To Pay (WTP) Matrix (sample figures only)

[1] Source: http://siteanalytics.compete.com

I am in fact glad to glance at this weblog posts which consists of lots of useful facts, thanks for providing these data.