In this post I’ll elaborate on Qualcomm’s strategy to unbundle technology licensing from selling chipsets in contrast to how Intel does it. Intel’s business model is to sell chipsets bundled with technology licenses. In Qualcomm’s case, a mobile device vendor can use chips designed by companies other than Qualcomm which still incorporate licensed Qualcomm technology. Further, this post attempts to analyze the competitive strategies in the wireless technology and standards industry. The 3 key areas of discussion in this brief are licensing strategy, competitive strategies for Qualcomm’s competitors in the mobile chipset market and new market entry with technology and standards.

Qualcomm adopts a business model such that value capture is achieved in two ways:

- By outsourcing chipset manufacturing and then subsequently selling the chipsets to device manufacturers. This makes up 63% of Qualcomm’s overall revenue

- By IP licensing, which makes up 27% of Qualcomm’s overall revenue. It relies on patents for licensing revenue, which are used to fund its R&D investments for next generation telecommunication technology such as 3G CDMA standards and development of OFDMA-based 4G standards[1].

Strategically it is more valuable to bundle two or more loss-makers and to unbundle two or more profitable products. For Qualcomm, technology licensing and ASICs (chipset) manufacturing could both separately be profitable endeavors. Qualcomm was able to charge CDMA licensees ongoing royalties, and sometimes upfront payments for development support, for the use of its patented technologies (in the realm of about 5% of ASP) in manufacturing and selling CDMA based products.

Qualcomm was selling CDMA licenses and chipsets to the entire value chain. It would sell CDMA licenses to network operators like PacTel, and it would sell chipsets to handset manufacturers like Kyocera, who purchased Qualcomm’s handset division[2].

Another reason why Qualcomm unbundled licensing from selling chipsets was that the major industry bodies- the FCC, CTIA and TIA- would more likely favor CDMA if it was perceived as a fragmented market[3]. Had Qualcomm chosen to sell the chipsets to device vendors that could not use chips designed by companies other than Qualcomm, it might have been perceived as exacting too much control over CDMA rendering the latter a less likely choice for a standard.

While the technology licensing made Qualcomm very good money, with very high margins and continues to do today, royalty costs became a sticky issue with handset manufacturers. Intense competition in a maturing wireless market hurt the manufacturers who decided to pursue non-proprietary standards such as the case with Intel’s PCG that chose the TDMA-based GSM.

Early in its life Qualcomm ensured it retained significant market power, justifying the strategic decision to work with a network of licensees for its technology portfolio while selling chipsets to wireless and phone manufacturer.

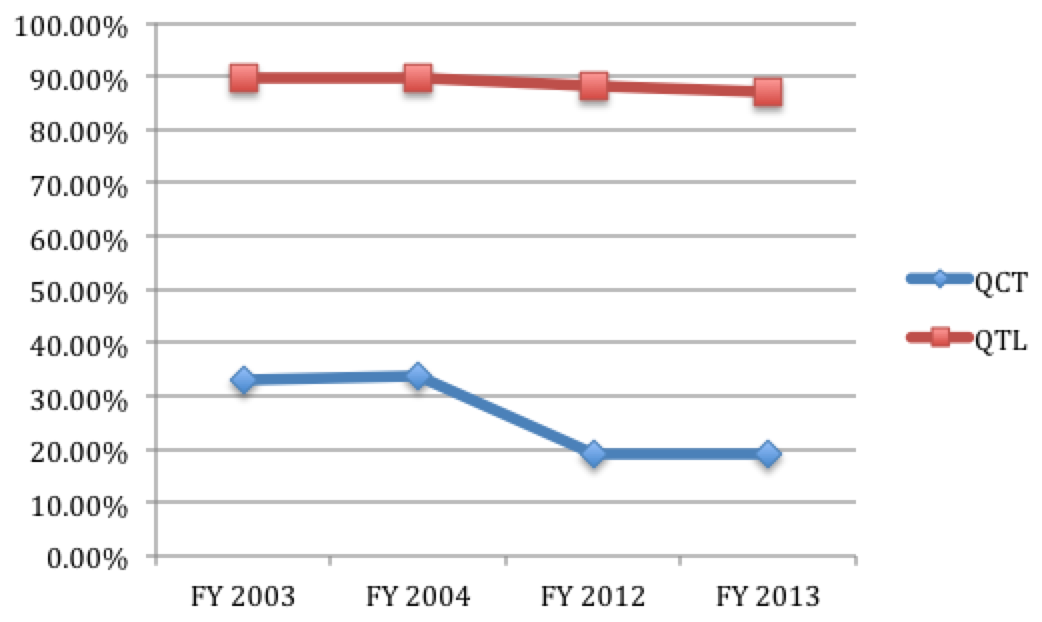

By 2004, income before taxes of the division making and selling integrated chipsets and software to both wireless phone and infrastructure manufacturers, QCT (division that manufactures equipment and sells chipsets) comprised over 45% of total income before taxes, a YOY growth of 23.6%[4]. QTL (the technology licensing division) contributed 51.6% of total income before taxes in 2004, a YOY growth of 24.93%. Historical gross margins for QCT and QTL are summarized below:

Figure 1: QCT & QTL Gross Margin Trend (2003-13)

Notice the decrease in the margins for QCT over the decade. Qualcomm explained that this decrease in QCT gross margins as a percentage of revenues in FY 2012 was primarily due to an increase of 33% in R&D expenses and SG&A expenses, and decrease of gross margins in FY 2013 was due to the net effects of lower average selling prices and unfavorable product mix[5]. However, this drop in margins is not surprising given that the cellular handsets market has grown extremely cost competitive. The table below shows the cumulative decline in Average Selling Price for the worldwide wireless phone industry over a 9-year period[6]:

| 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | |

| ASP | – | -5% | -12% | -17% | -23% | -23% | -25% | -27% | -28% |

Table 1: Cumulative Decline in ASP

Note: Reduced margins resulting from declining ASPs are somewhat offset by the growing mobile user population.

Let us now detail what the implications for companies such as Intel and Broadcom that are attempting to enter and compete in the mobile chipset market. Generally speaking, companies attempting to enter and compete in the mobile chipset market need to identify gaps in technology portfolio and fill those gaps either with in-house manufacturing, inbound OEMs or acquisitions of firms specializing in the production and support of missing technologies. Entering the wireless market almost mandates the following strategic elements be in place first:

- Complete Technology Solution: this would ensure the entrant is able to complete on an equal footing with incumbents and other entrants (e.g. Intel vs. TI)

- Joint Ventures and Partnerships: the entrant must be able to forge strategic relationships with value chain participants such as with leading handset manufacturers to ensure the selected business strategy ensures profitability and market power (e.g. ODM-to-operator plus partnership with leading handset manufacturers)

- Volume Economics: lower per unit costs are achieved using open standards

- Emerging markets: partnering with handset manufacturers and data operators to gain market share in China and India that have a combined 1.6B phone users[7].

However, not all strategic goals listed might be achievable due to constraints in the market such as competition from incumbents, prohibitive cost-basis for building technical capabilities necessary to compete and inability to forge long-standing relationships with participants in the mobile phone value chain.

Complete Technology Solution

Intel needs to identify what technologies it lacks in the portfolio and move to fill the gaps. For example, early on it knew that baseband processing was something it lacked while Texas Instruments was the market leader in baseband processing. It was easier for TI to acquire ARM core technology via licensing than it was for Intel, which already had the license to use ARM core, to build baseband-processing capability. Therefore Intel decided to acquire DSPC to complete its technology stack needed to compete in the mobile chipset market.

Joint Ventures and Partnerships

When Intel made entry in the non-cellular capable Personal Digital Assistants (PDAs) market it was hampered by cell phone manufacturers that smartly started incorporating PDA capabilities in smartphones. The new data-capable cellular networks that network operators were able to build further boosted the cell phone manufacturers. Incumbent mobile chipset and handset manufacturers had much stronger relationships with the operators that owned the data-capable networks.

A viable strategy for companies like Intel and Broadcom is to explore alternate paths to market entry, such as Original Design Manufacturer (ODM)-to-operator. In the ODM-to-operator model, Intel could manufacture chipsets for the ODMs to then optimize for cost and manufacture mobile phones for sale to the network operators. The network operators would then subsidize the cost of the phone in return for a service contract from the end user.

Chipset development can be a high cost endeavor if the company chooses to manufacture them. On the other hand, choosing the ODM-to-operator strategy can only be successful if the company enters into a relationship with leading handset manufacturers to ensure volume targets that are needed for reducing cost basis are reached, and sustained. Successful entry into emerging markets depends on the success of the strategies discussed above.

Finally, worth mentioning are the implications for companies attempting to introduce new cellular technology standards (think WiMAX). In my view, the key success factors for a company’s go-to market strategy when introducing a new cellular technology seem to be:

- Ecosystem supporting the new technology

- Choosing open standards

Additionally, companies introducing new technologies to the mobile industry need to also ensure they execute on each of the strategic elements in their go-to market strategy.

Ecosystem

Equipment manufacturers, cable companies and mobile operators form the value chain for cellular technology. It is vital to get commitment upfront from network operators that hold the most attractive spectrum before striking deals with equipment manufacturers to put the new WiMAX or FLASH technology in their devices.

Open Standards

Intel with WiMAX and other companies introducing new cellular technologies has a strategicdecision to make: deliver products based on proprietary technologies or back an open standard. The open standard is widely available to any equipment maker meaning the entrant will have to deal with competitors, however, market innovation will be high and if the right mix of product line and service line strategies are chosen, might even result in differentiated products that command price premiums.

Another key factor favoring open standards is the enabling of global economies of scale and decreasing costs. Complete standardization results in high volume of chips in the market that are based on this open standard, and therefore could be used inside the devices of every device manufacturer. The chip manufacturer gets to produce a high volume of chips thereby spreading fixed costs over a large number of units ultimately resulting in a lower per unit cost.

That’s all folks. Hope you enjoyed the post.

[1] Qualcomm 10-K, Nov 2013, http://tinyurl.com/n63vw6d

[2] Page 14, Intel in Wireless in 2006 (A): Tackling the Cellular Industry SM-165

[3] Page 168, Chapter 15, The Qualcomm Equation, Dave Mock

[4] Qualcomm 10-K, Nov 2004, http://tinyurl.com/lsgguy2

[5] Qualcomm 10-K, Nov 2013, http://tinyurl.com/n63vw6d

[6] “Qualcomm, Inc. 2004”, HBS Case. Data derived from Exhibit 5.

[7] Technology Intelligence & IP Strategy, http://tinyurl.com/mohl3z9