Background

ABC is a hypothetical voice data processing company that has created technology to secure voice transactions. The worldwide market opportunity is approximately $5B-$7B. ABC is asking for $8M to enter the US and Australia markets, and develop the next generation of their products.

Overall Investment Decision and Explanation

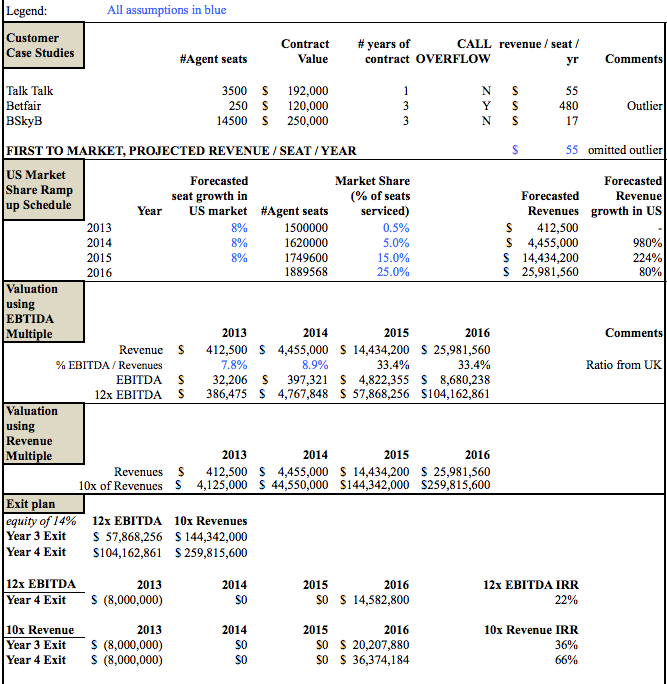

Our investment decision is to invest $8M with a minimum 14% in equity in ABC in 2013. ABC is expected to attain 25% share of market by year 4 (2016). Using the EBITDA multiple approach, projected valuation for Year 4 is $104M with an IRR of 22%. Using the 10x Revenue multiple approach, projected intrinsic value of the firm for Year 3 is $144M with an IRR of 36%, and for Year 4 projected valuation is approximately $260M with an IRR of 66%. Using either approach, exiting in Year 4 meets and exceeds our stated exit objectives, although the 10x Revenue multiple is more aggressive and will need to be examined in more detail using precedent valuations in the US market. With their proven business model, sound business plan, and untapped market potential we felt there is a high probability to receive a 3x-4x return on our invested capital.

Valuation Process

To estimate the current value of the company, we need actuals to date data, however their 2013 year end forecast would suggest a $66M value based on 10x of expected revenue. In lieu of the actual data, we focused on the future value using a bottom-up valuation approach where we estimated ABC’s revenues using their UK contracts as proxies. Assuming a British Pound to US Dollar conversion rate of 1.6 to value the contracts in US dollars, we arrived at desirable Year 3 and Year 4 firm valuations using a 10x Revenue multiple. Next, we also used the 12x EBITDA multiple method with EBITDA/Revenues ratios taken from UK forecasts as inputs into our financial model. With this method we arrived at a desirable exit in Year 4.

Expected Return

We benchmarked invested capital returns for VC firms and noted variance in expectation from seed to series D and beyond. The later the round, the lesser the upside for expected return. With this process in mind for a series B investment in Semafone, we expect a minimum of 3 to 4x, or approximately $32M in return. From our valuation due diligence we expect the return to be in the range of $40 to $70M.

Details

Thanks for reading!